Pompey have published their Annual Accounts for the 2024-25 season and here’s the PST analysis of what the numbers mean. You can download a copy of the club accounts here: https://www.portsmouthfc.co.uk/news/2026/march/18/statement-of-accounts/

Usually, I take this opportunity to thank Tony Brown for answering my questions. However, Tony left the football club in October so I would like to say a few words about Tony’s time at the club. Tony Brown joined the club in the 2013-14 season as the PST and Presidents took on the enormous task of bringing the club out of administration.

In particular, he was instrumental in ensuring that all the legacy debt from administration was paid off early and thus helped to create a financial platform that enabled Paul Cook to lead the club to promotion as League 2 champions.

After the club was sold in the summer of 2017, Tony managed the finances of the club with care, balancing the demands of funding the playing squad and investing in the stadium and training ground.

He was always helpful with our annual review of the accounts and throughout our frequent chats over the seasons, and I wish to pay tribute to his contribution to PFC.

This year, I’d also like to thank Andy Cullen and Tanya Robins for an advance copy of the accounts and for helping me with this review. Additionally, I’d like to welcome Ronan Callaghan into his new role as Chief Financial Officer, and I look forward to engaging with him on PFC finances in the coming months.

Introduction

These accounts cover the 2024-25 season, Pompey’s first season back in the Championship since 2011-12. The accounts show how revenues and wages have increased in the second tier of English Football and how the funds provided by the owners have been focused more on the football operation after several years of focussing on infrastructure.

They also show a significant change in the funding mechanism used by the owners to inject funds into the club. This may be controversial for some fans, and I will go into the reasons for this change.

Strategic Report

The Strategic Report is the section of the accounts where the Directors set out the key events of the year and give context to the numbers in the other sections.

Once again, the club has expanded the length of this section, from 9 pages to 10 pages. I’m pleased to see the club give more information about how the club operates than many clubs at our level and higher.

I recommend that everyone should read this section to get a picture of how the Club’s executive team saw the season, even if the numerical sections of the accounts are not of interest.

Topics covered in this narrative explanation of the season include:

- Football Performance

- The Academy

- Pompey Women

- Fan Engagement

- The Club’s Vision and Purpose

- Fratton Park Redevelopment

- Pompey Health & Fitness Club and the Training Ground

- Trading Performance and the Balance Sheet

- The Club’s environmental impact and sustainable working projects

Cash – where it comes from and how it’s spent

Rather than look at the Profit and Loss account as I have in previous years, I’m going to focus on cash.

Profit and Loss is becoming decreasingly relevant in the context of football clubs. Pretty much all football clubs make a loss. Even if they have a year when they sell players for huge profits, over the medium to long term they lose money.

In fact, it’s arguable that fan expectations prevent clubs from making profit. Every £1 of profit retained by a club is viewed as a £1 less that could be spent on wages. And if a club were to make a profit and then pay a dividend to the owners then this would cause uproar in most club fanbases.

Therefore, I’m going to focus on cash. Where it comes from and where it is spent. Cash is the ultimate key resource of a club. Clubs can exist for years making losses, but if they run out of cash then they soon start to tumble down the leagues or ultimately go into administration.

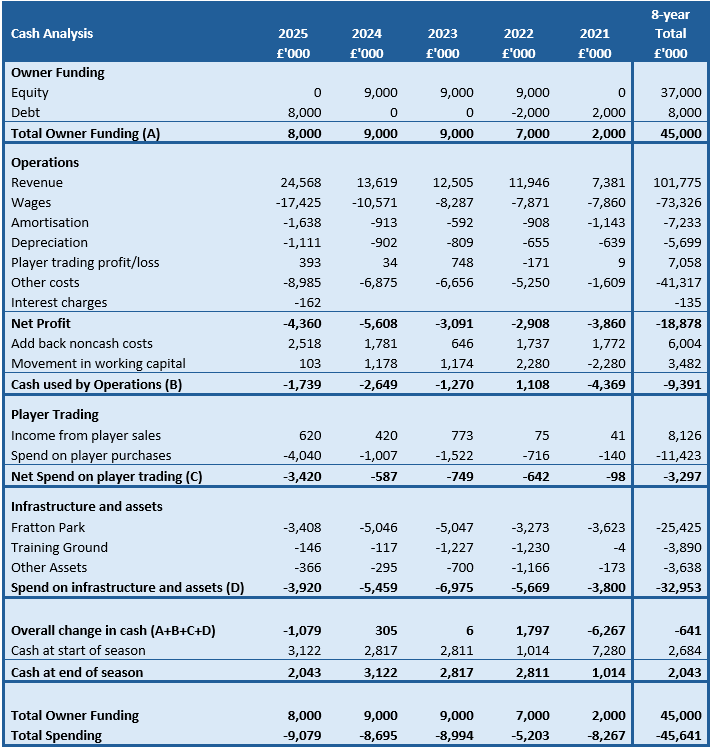

The following table shows the cash in and out of the club over the last 5 years and in total in the 8 years of Tornante ownership

I’m conscious that this is a very number heavy table, so I’ll break it down section by section, starting with Owner funding.

Owner Funding

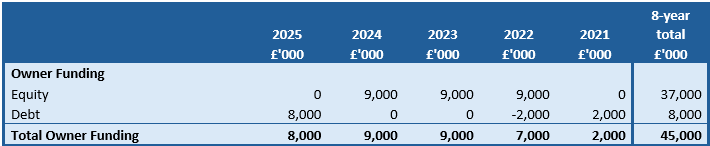

The standout here is the switch from funding via equity to funding via a loan.

Given our history prior to fan ownership, this is a change that may cause concern to many fans. Both the PST and President members of the Heritage and Advisory Board recognised this. We questioned both the club and Michael Eisner extensively about the reasons for this change and the future intentions.

Everyone will have seen the recent announcement that as part of succession planning, Michael Eisner has transferred 73.5% of his shareholding in Pompey to his sons Eric, Breck and Anders. However, funding for the club is still coming from Michael Eisner, and if this continued to be done via equity then it would change the percentages held by Michael and his sons. Therefore, funding will now be provided by loan.

The US IRS (their version of our HMRC) mandates that any loans to a company from a related party must carry interest to qualify as a valid loan. The interest being charged is at the minimum level permitted by the IRS – currently approximately 3.6-3.7%. This interest is not being physically paid by the club and is instead being added to the loan. Additionally, the IRS requires that loans must have a repayment option on them to be treated as a loan and not an investment.

We asked Michael directly about his intentions with this loan. We have been informed that there is no intention to require this loan to be paid at the present time, or before the club has the resources to pay it without negatively affecting club operations.

An important distinction is that there remains no external debt, and the club is not beholden to any third party lenders.

That presents the facts about the switch in funding method. I will return to the subject of the switch to debt funding later in this review to look at the risks to the club and whether this gives any cause for concern on sustainability.

Overall, however, we can see that at the end of the 2024-25 season the owners had provided £45m in funding since they bought the club in 2017. The accounts also disclose that a further £9m has been provided since these accounts up to the end of December 2025.

Operations

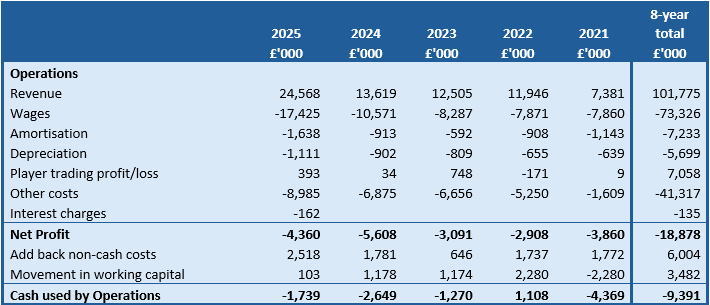

This section of the cash analysis looks at the cash losses that arise from the Profit and Loss. The income from revenue and how the costs outstrip it, using up some of the owner funding.

The first section of this table shows the Profit and Loss for the club. I’ve then added two rows that adjust it to remove the costs that are non-cash, and the effect on cash of changes in working capital.

Non-cash costs are amortisation, depreciation, the profit on player trading, and the interest charged on the owner loan which is being added to the loan. Amortisation is writing off player transfer fees over the length of their contract. For example, if a player is signed for £1m on a 2-year contract then his amortisation is £500k per year.

Depreciation is similar but for assets such as the stadium, or gym equipment or cars. The cost of the asset is written off over the expected life of the asset.

We also adjust for the movement in working capital. Working capital is the showing of the timing differences between the revenue and costs in the season and when the money is actually paid or received. This is predominantly the impact of receiving season ticket money in advance of the following season. We can see here that in the post-covid period after 2021-22, advance season ticket payments grew as the season ticket demand and prices increased. In the 2024-25 season it has hardly changed this means that the advance season tickets payments received in May/June 2025 for the 2025-26 season are very similar to the amount received in advance in the previous season.

I’ll take an overview of the P&L for a moment before narrowing down on revenue and wages.

What we see is the large increase in revenue in the Championship, and a consequent increase in wages. However, the wage bill did not increase by the same proportion. This is perhaps reflected by a much higher net spend on player acquisition as we will see in the next section.

Amortisation grew sharply due to the growth in transfer fee spend as the first year of the contracts for the new signings was written off.

The Other Costs also grew significantly, and this was primarily due to an increase in the spend on fees for loan players. This cost of loan players does not go into wages as they are not employees of the club.

The fact that the club made a smaller loss in the Championship may seem counter intuitive. The amount of cash required to cover operations also decreased, although by not as much. This will reflect the fact that although the money received from the EFL increases significantly, lots of costs for the club will not have changed, or will have had a lower percentage increase. For example, business rates, electricity, admin salaries will not have increased 80% just because revenue did.

Overall, over the 8 years of Tornante ownership, the club has made cumulative losses of nearly £19m and, when you exclude depreciation and amortisation, this has needed £9m of cash to fund it.

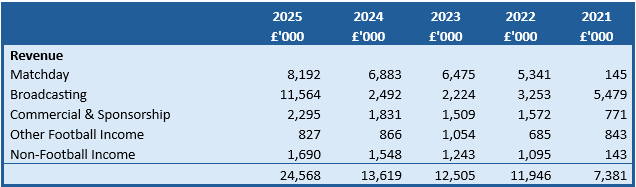

Turning to revenue:

Overall revenue grew by £10.5m in the year. Promotion to the Championship drove the broadcasting income up sharply from £2.5m to £11.5m. The rest of the increases came from increased ticket prices and higher income from sponsorship, catering and merchandise.

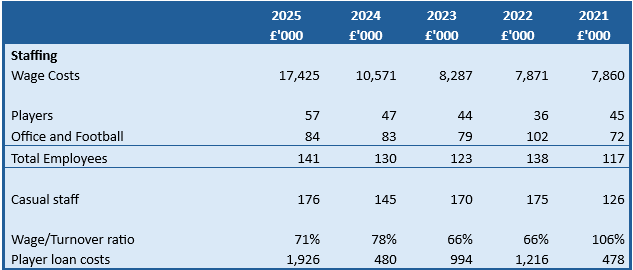

Moving on to wages, we see that the wage bill grew sharply from the previous season, with an increase of close to £7m in wages. This saw the playing staff element of this cost more than double in the season compared to League 1.

After a couple of seasons of reducing loan player costs, we see a sharp increase in loan player spend. This reflects the higher costs of loan players in this division compared to League One and the higher revenue allowing more to be spent. In particular, the loan signing of Freddie Potts was an example of this increase being put to good use.

The number of staff increased slightly, mainly on the playing side. We can see that the wage bill did not increase in proportion to the increase in revenues. However, we should also consider the cost of loan players when assessing the change in wage costs. The combined costs of Wages and loans shows a 75% increase from the previous season versus an 80% increase in revenue, so total personnel spend was broadly increased in proportion to revenue.

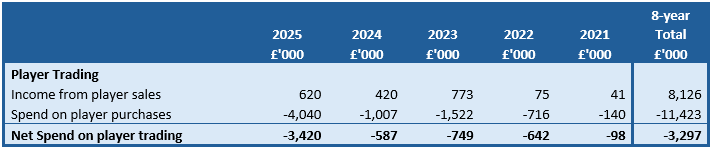

Player trading

An increasing importance has been placed on Player Trading by the club in its public discussions on strategy.

In the last season we saw a significant increase in the net player spend. In fact, it reversed a net income from the previous 7 seasons.

This season saw the club sign the following players

Overall, the commitment to funding an increased player acquisition budget must be welcomed. It must also be hoped that this will not only continue but will increase further. It represents, perhaps, the best chance that Pompey has to stabilise in the Championship and challenge in the upper half of the table. One only has to look at the example of Coventry City to see a club that have leveraged player trading to potentially great success in 2025-26.

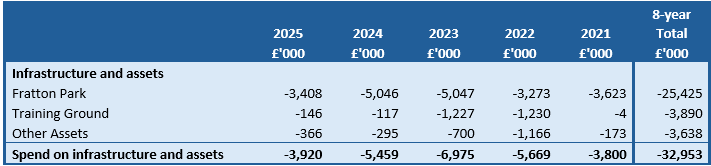

Infrastructure and asset spending

There was still heavy spending on Fratton Park in the season. This saw the new TV gantry being installed, the mezzanines in the North Stand and the refurbishment of the Victory Lounge. Additionally, a TV studio was constructed with a new media centre in the corner between the Milton End and the South Stand.

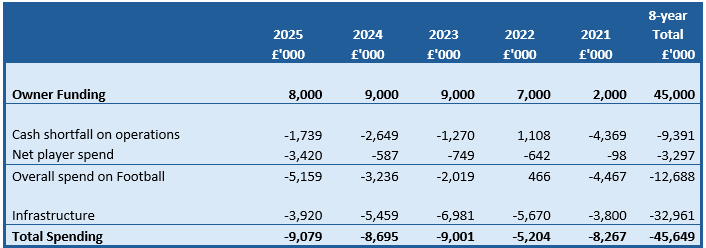

The overall picture

Summarising all of this spending we can see the overall pattern of funding and spending

Both the 2020/21 and 2021/22 seasons were impacted by Covid. Additionally, they were in part funded from the original £10m that Tornante put into the club in 2017 when they bought it.

However, in the three years since then, the overall spending has remained consistent. What we can see is that last season the priority for this spend and the owner funding switched from infrastructure to the football spend. And although the player wage bill did not increase in line with the higher level of TV money, the owner funding was instead used to fund player acquisitions.

Looking at the cumulative 8 years, we see that Tornante have provided £45m of funding to the club. This has been spent on £33m of infrastructure improvements, £9m was used to cover the cash cost of the losses, and a net £3m has been spent on players.

Balance Sheet

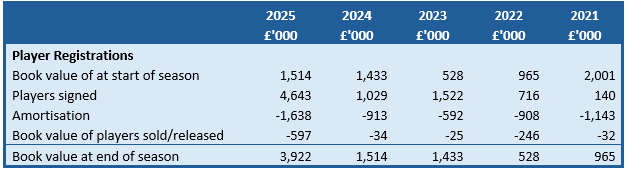

I’m not going to go into huge detail on the Balance Sheet and will just focus on two areas – Player Registrations and Liabilities.

The Book Value of the squad refers to the accounting value placed upon it. The accounting industry rules on valuing players in club accounts are that they can only be valued at what they cost to sign, less the amortisation that has been applied by the end of each season. This means that the book value of the squad does not reflect market value – ie players that came from an Academy are valued at zero as they did not cost anything to sign. Likewise players signed for modest fees who gain value are also undervalued .

Eagle-eyed readers may spot that the number in the above table for players signed does not tally with the numbers for cash spent on new players in the earlier section of this report.

This is because of the impact of staged instalments on transfers. The cash spent will include instalments on players bought in previous seasons and won’t include instalments to be paid in future seasons.

The amounts above shown as players signed represents the value of all the signings made in the 2024-25 season including future payments that are known. It doesn’t include any sell on percentages or conditional payments for appearances, etc. So, the 10 players listed earlier as acquired for a fee will cost a combined £4.6m, plus any future conditional amounts.

Moving on to liabilities, the club’s overall liabilities grew from £11.4m in 2023-24 to £20.7m. The majority of this being the owner funding injected as a debt.

One point worth noting is that in the Debtors of the club a sum of £700k is noted as being owed by Portsmouth Women’s Community Football Club – The Pompey Women’s team. This is for funding to the women’s team that was paid via the men’s team. Future funding for the women’s team has been paid direct to the separate company that runs the Women’s team, and a note to the accounts makes it clear that in the 2025-26 season the loan from Tornante was reduced by the amount the Women’s club owes the men’s so that each club is carrying the debt relating solely to its own activities.

We continue to have no liabilities from the kind of high-risk lending firms that are widespread around football, or any other third parties that could trigger a crisis.

Summary of the 2024-25 season

The headline story of these accounts is undoubtedly the change in the funding model from equity investment to loan funding. This will understandably give cause for concern to many fans after our club’s past difficulties.

As I previously mentioned we have asked extensive questions about this change, and I’m pleased to say that Michael Eisner has responded in open and frank ways about the reasons for doing this. We are naturally reluctant to discuss the personal affairs of the owners in this way, but the change to the funding model is of sufficient importance to override this and without explaining these reasons it would naturally raise questions about them.

The reasons given for the change in funding model are credible and understandable. By gifting ownership of 73.5% of the club to his sons, Michael Eisner is starting the succession plan for his personal wealth and the longer-term future of the club. It is likely that it may also help to reduce future tax liabilities relating to his ownership of the club that could be very large.

However, the club requires continual funding from Michael Eisner and thus, to preserve the balance of ownership, funding will be made via a loan from him for the foreseeable future. The accounts confirm that the interest charge is at the lowest level allowed by the US IRS, and that it is not being physically paid in cash. The interest rate is well below the commercial interest rate that the club would pay if it borrowed from a high street bank, let alone the higher rates that the specialist football lenders charge. And the debt is not secured against any assets of the club.

Having understood the reasons for this change, we’re left with the question: does this increase the risk on the club?

And to this I would say not in any meaningful way.

Equity is the safest form of investment as it can never be asked to be repaid. Funding by loan does carry the potential that repayment is requested. However, the club still must have the resources to repay it and to do so without them would almost always trigger a crisis and likely administration which would result in the owner losing control of the club. I cannot think of any occasion where an owner has requested repayment when they are continuing to fund the losses and player acquisitions. Most often, the owner converts the debt into shares at a future date.

In addition, and key to this assessment of risk, the debt to the owner is not secured against any assets. It means that there is no advantage to be gained from calling in the debt and everything to lose. In an administration the debt would rank equally with the general creditors and behind HMRC and the players. Our past difficulties stemmed from owners who secured their debt against the stadium and other assets of the club, giving them total control of the administration process.

The provision of funding via loan is primarily to ensure that that the balance of ownership between Michael and his sons remains at a constant proportion. I’m aware that similar structures are used in UK family-owned businesses to reduce Inheritance Tax. In order to satisfy the US IRS requirements, the owner loan must have all the conditions on interest and repayment that a normal commercial loan would have. Whether or not repayment is ever requested is up to the owners and they have confirmed that the loan would not be repaid unless the club has the spare cash to do so. I see very few scenarios where that would be possible.

Regardless of whether funding is provided by equity or loan, the club needs continual funding by the owners. We have received assurances that the owners remain committed to future funding.

The accounts disclose that a further £9m has been advanced to the club in the current season, so the commitment to future funding is being upheld. I fully expect that this funding will exceed £10m and be heading toward £14m by the end of the season.

The core risk to the club continues to be if Tornante should decide to stop their funding for some reason. This would be the core risk whether funded by equity or loan and we have no reason to believe that the funding will stop.

Having discussed this in detail with the club and with Michael Eisner, I feel that I have a good understanding of the reasons for the switch in funding method and his future intentions. The transfer of assets as a gift is a common practice in the UK to reduce Inheritance Tax. From the earliest discussions in 2017, the Eisner family have said that their ownership is a family affair. Therefore, the club was always going to pass from Michael to his sons one day, and this action starts that handover process.

For the reasons explained above, I don’t believe that the switch to unsecured owner debt increases risk on the club by any meaningful amount. The unsecured nature of the debt conveys no advantage to the Eisner family in requesting repayment and would mean any form of administration would cause them significant losses. The method of funding does not alter the core risk of operating as a football club with a negative operational and asset cashflow, covered by owner funding. Negating that core risk is not possible if the club is to operate at the level of the football pyramid that fans expect.

Beyond the issue of the funding, the accounts show the change in emphasis from funding infrastructure to funding player acquisition. 10 new players were signed for fees totalling £4.6m in the season and we wait to see which ones will develop into saleable assets that will enable the trading model to fund growth in the wage budget.

Looking forward to 2025-26 and beyond

Last season I raised the question of what model the club wanted to follow. We can now see what model that is.

There was a step up in the player acquisitions last season, and we saw in the summer of 2025 that this continued into this season with spending set to exceed last season’s amount. Last year I raised the risk of relegation while the club waits for this to deliver results. Clearly last season the club managed to avoid this without having to incur huge operational losses.

Michael Eisner asserted that the club would not be relegated last season and has done so again this year. The fact that we sit close to the relegation zone in the league table demonstrates that risk. Clearly there will be an onus on the owners to provide the coaching team with the resources they believe they need to survive each season, along with the resources to ensure that the player trading model starts to deliver.

Football in the Championship is broken, however. Spending big in the summer doesn’t guarantee success, and research has shown the link between wage spending and points won to be particularly weak in the Championship.

Teams get the same money whether they finish 7th or 21st, so from a cold business point of view spending big to finish 8th to 12th just guarantees huge losses compared to controlling spending and finishing 16th to 20th.

As fans, however, the experience and emotion of watching those two options is very different.

The new Independent Football Regulator may help to bring in a more level playing field. It may make clubs act and spend more responsibly. But any impact it may have is some time away. Additionally, any impact it has on profligate spending will focus on ensuring that spending matches revenue.

That would then bring attention back to Pompey’s capacity to generate revenue, with questions regarding the stadium capacity and facilities. It will also bring attention to the club’s academy and development structures, and how they can be developed so that we are producing a regular stream of high-quality saleable players that will boost our ability to sign better players and match their wage expectations.

Last year we asked fans whether they preferred controlled spending or higher losses and the answer was clear in favour of controlled spending. Anecdotally, there appears to be a growing desire to see more funds invested in the playing squad to pull us away from being relegation candidates and to deliver players that may be developed into future assets that could provide transformational funds to the club.

We will continue to check on fan preference and continue our dialogue with the owners on their strategy and the future of the club.

In the meantime, please feel free to give your feedback to us at [email protected].